Most people think a quick scrub and some store-bought spray is enough to keep their bathroom clean. It looks fine. It smells okay. So it must be hygienic, right? Not exactly. Bathrooms are hotspots for bacteria, viruses, and mold. They are the perfect breeding ground for germs, especially in tight spaces and hard-to-reach corners. While regular cleaning does help, it often misses the deeper grime. That is where professional bathroom cleaning steps in. In 2025, more homeowners are recognizing that a clean-looking bathroom is not always a healthy one. Below is a look at reasons it is advisable to get professional cleaning services for your bathroom.

They Reach What You Cannot See or Touch

There is a limit to what a mop, sponge, and over-the-counter cleaner can do. Professionals go far beyond the surface. They are trained to find the buildup hiding behind toilets, under sink edges, deep in grout lines, and inside drains. These are areas where bacteria thrive. If you ignore them long enough, you end up with odors, discoloration, and even mold spores in the air. Professionals use high-grade tools that break down mineral deposits, kill bacteria, and remove soap scum at its root. They also understand how different surfaces respond to different products. One wrong cleaner can ruin tile or corrode fixtures. That kind of damage costs more in the long run. Professionals get it right the first time. And because they work efficiently and thoroughly, they often finish a job in half the time it takes a homeowner to do a halfway clean. What you are paying for is expertise, not just effort.

It Helps Keep Your Family Healthier

Bathrooms are shared spaces. That means whatever bacteria one person brings in can quickly spread to everyone else. From toilet handles to faucets and even the floor, every surface is a potential transfer point. Especially in homes with young kids, elderly family members, or anyone with health concerns, hygiene matters more than ever. Regular cleanings help, but only up to a point. Professional cleaning adds another layer of defense. It reduces allergens, eliminates mold at the source, and kills bacteria that standard products might miss. That can lead to fewer colds, fewer allergic reactions, and a generally safer space for daily routines. It is not about being overly cautious. It is about reducing risk. With all the germs we encounter outside, your bathroom should be the one place that resets your sense of cleanliness. A professionally cleaned bathroom helps make that possible.

It Saves You Time and Headaches

Let’s be honest. Most people do not enjoy deep cleaning their bathroom. It is one of those chores that gets pushed down the to-do list until it becomes unavoidable. And by then, it takes even longer. Hiring a professional turns a dreaded task into a solved problem. It frees up time for things you want to do. It also saves you from second-guessing your results. No more wondering if the shower is clean or if the sink just looks better under certain lighting. You can rest easy knowing it is been handled properly. Some people worry about the cost, but compare that to the value of your time, your peace of mind, and your family’s health. For many, it is a simple decision. Once you experience a truly …

A Precious Metals IRA provides an opportunity to diversify your retirement portfolio, reducing the risk associated with inflation. Precious metals have historically exhibited a low correlation with traditional asset classes, such as stocks and bonds. Therefore, including precious metals in your IRA can help offset potential losses in other investments during inflationary periods, enhancing the overall stability of your retirement savings. Inflation poses a significant threat to the purchasing power of your retirement funds.

A Precious Metals IRA provides an opportunity to diversify your retirement portfolio, reducing the risk associated with inflation. Precious metals have historically exhibited a low correlation with traditional asset classes, such as stocks and bonds. Therefore, including precious metals in your IRA can help offset potential losses in other investments during inflationary periods, enhancing the overall stability of your retirement savings. Inflation poses a significant threat to the purchasing power of your retirement funds.

Another common ergonomic issue is having your computer monitor too high or too low. Generally, the top of your monitor should be at or slightly below eye level. This helps to reduce strain on your neck and shoulders. If your monitor is too low, consider using a monitor riser or elevating it with a stack of books. If it is too high, adjust your chair’s height to bring your eyes to the correct level.

Another common ergonomic issue is having your computer monitor too high or too low. Generally, the top of your monitor should be at or slightly below eye level. This helps to reduce strain on your neck and shoulders. If your monitor is too low, consider using a monitor riser or elevating it with a stack of books. If it is too high, adjust your chair’s height to bring your eyes to the correct level.

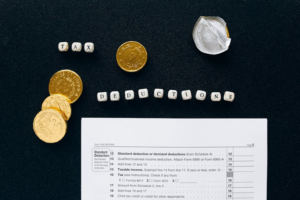

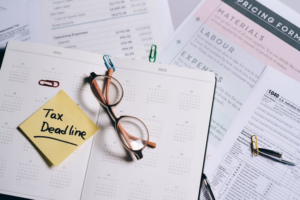

Most tax preparers offer a variety of services that can help you get the most out of your return. They’ll be able to suggest tax-saving strategies, find deductions and credits you might not have been aware of, and help you file for all the rebates or refunds you’re eligible for. So if you want to maximize your refund, it’s a good idea to enlist the help of a tax preparer.

Most tax preparers offer a variety of services that can help you get the most out of your return. They’ll be able to suggest tax-saving strategies, find deductions and credits you might not have been aware of, and help you file for all the rebates or refunds you’re eligible for. So if you want to maximize your refund, it’s a good idea to enlist the help of a tax preparer. Filing taxes can take up a lot of your time and energy. If you don’t have the luxury of extra hours in your day, it might be best to hire someone who can do it for you. A tax preparer will be able to get your taxes done quickly and efficiently, so you can spend more time on other things.

Filing taxes can take up a lot of your time and energy. If you don’t have the luxury of extra hours in your day, it might be best to hire someone who can do it for you. A tax preparer will be able to get your taxes done quickly and efficiently, so you can spend more time on other things.

The first and foremost step in SEO is to determine the keywords your potential customers use to search for products related to pet stores. Identifying keywords and phrases will help you optimize your website for those terms. You can use tools like Google Keyword Planner or Ubersuggest to research relevant keywords. Once you have identified the right keywords, use them to optimize the content on your website. This includes using the correct phrases in titles and meta tags, as well as including them within the body of your text.

The first and foremost step in SEO is to determine the keywords your potential customers use to search for products related to pet stores. Identifying keywords and phrases will help you optimize your website for those terms. You can use tools like Google Keyword Planner or Ubersuggest to research relevant keywords. Once you have identified the right keywords, use them to optimize the content on your website. This includes using the correct phrases in titles and meta tags, as well as including them within the body of your text. Reviews and comments are an essential part of your pet store website, as they give potential customers a glimpse into the satisfaction level of previous customers. Therefore, do your best to encourage reviews and interaction on your website. This can be done by actively responding to comments and reviews or even by providing an incentive for customers to leave a review.

Reviews and comments are an essential part of your pet store website, as they give potential customers a glimpse into the satisfaction level of previous customers. Therefore, do your best to encourage reviews and interaction on your website. This can be done by actively responding to comments and reviews or even by providing an incentive for customers to leave a review.

The motor power is one of the most important things to consider when choosing a vacuum cleaner. This is because the motor is responsible for providing the suction power that helps to clean your floors. The higher the wattage, the more influential the vacuum will be. However, you also need to consider the size of your home. You will need a vacuum with more powerful suction if you have a large house. On the other hand, if you have a smaller home, you can get away with a less powerful vacuum.

The motor power is one of the most important things to consider when choosing a vacuum cleaner. This is because the motor is responsible for providing the suction power that helps to clean your floors. The higher the wattage, the more influential the vacuum will be. However, you also need to consider the size of your home. You will need a vacuum with more powerful suction if you have a large house. On the other hand, if you have a smaller home, you can get away with a less powerful vacuum. Another vital thing to look for in a vacuum cleaner is the filtration system. This is because the filtration system is responsible for trapping dust, dirt, and other allergens. If you have allergies or asthma, you will want to ensure that the vacuum cleaner you choose has a sound filtration system.

Another vital thing to look for in a vacuum cleaner is the filtration system. This is because the filtration system is responsible for trapping dust, dirt, and other allergens. If you have allergies or asthma, you will want to ensure that the vacuum cleaner you choose has a sound filtration system.

The earliest recorded instance of the smoking jacket dates back to King Charles II, who is said to have popularized the garment in the 1600s. It is believed that the king adopted the style from Persian nobility, who wore similar robes while indulging in their hookahs.

The earliest recorded instance of the smoking jacket dates back to King Charles II, who is said to have popularized the garment in the 1600s. It is believed that the king adopted the style from Persian nobility, who wore similar robes while indulging in their hookahs. The smoking jacket made a comeback in the 1990s. Designers such as Ralph Lauren and Calvin Klein created modern versions of the garment. These new jackets were often made of velvet or silk and were usually worn as part of a leisure suit.

The smoking jacket made a comeback in the 1990s. Designers such as Ralph Lauren and Calvin Klein created modern versions of the garment. These new jackets were often made of velvet or silk and were usually worn as part of a leisure suit.

It is crucial that you listen to your loved ones when they are talking about their mental health. It would help if you tried to be understanding and provide support for them. You can also offer to help them with things they may need assistance with.

It is crucial that you listen to your loved ones when they are talking about their mental health. It would help if you tried to be understanding and provide support for them. You can also offer to help them with things they may need assistance with. It is also vital to encourage your loved ones to seek professional help if they are struggling. This can be in the form of therapy, medication, or both. It is important to remember that mental health is just like physical health, and sometimes people need professional help to get better.

It is also vital to encourage your loved ones to seek professional help if they are struggling. This can be in the form of therapy, medication, or both. It is important to remember that mental health is just like physical health, and sometimes people need professional help to get better.

This is meant to cover funeral costs, outstanding medical bills, and any other debts or expenses that you may leave behind. While the death benefits are typically much smaller than a traditional life insurance policy, they can still provide your loved ones with much-needed financial assistance during a difficult time.

This is meant to cover funeral costs, outstanding medical bills, and any other debts or expenses that you may leave behind. While the death benefits are typically much smaller than a traditional life insurance policy, they can still provide your loved ones with much-needed financial assistance during a difficult time.

When you’re investing in stocks, it’s important to remember your goals. What are you hoping to achieve with your investment? Knowing this will help you make intelligent choices about which stocks to buy.

When you’re investing in stocks, it’s important to remember your goals. What are you hoping to achieve with your investment? Knowing this will help you make intelligent choices about which stocks to buy. One of the biggest mistakes people make when

One of the biggest mistakes people make when

Gasoline requires a great deal of energy to produce and creates pollution during refining. In contrast, biofuel can be produced with minimal fossil fuels and only requires crops to be planted in renewable soil.

Gasoline requires a great deal of energy to produce and creates pollution during refining. In contrast, biofuel can be produced with minimal fossil fuels and only requires crops to be planted in renewable soil. Gasoline can only be used in vehicles that are designed for it, but biofuels can be used in any vehicle without damaging the engine or other parts of the car.

Gasoline can only be used in vehicles that are designed for it, but biofuels can be used in any vehicle without damaging the engine or other parts of the car.

Sometimes in life, you can’t see the forest for the trees. When it comes to love, even people who are very intuitive may not be able to understand what’s going on in their own lives.

Sometimes in life, you can’t see the forest for the trees. When it comes to love, even people who are very intuitive may not be able to understand what’s going on in their own lives. Psychics can also wish you luck! Many people believe that good things start to happen when you surround yourself with positive energy. If you’re looking for a little extra help in this area, consider hiring a psychic to send you some good vibes and positive energy.

Psychics can also wish you luck! Many people believe that good things start to happen when you surround yourself with positive energy. If you’re looking for a little extra help in this area, consider hiring a psychic to send you some good vibes and positive energy.

Legalization is perhaps the main reason why CBD is currently popular. Without the recent legalization of cannabis for medical and recreational use, many current CBD users will not get CBD-infused products legally. Though there were some studies conducted on marijuana before its legalization, such studies were not well documented.

Legalization is perhaps the main reason why CBD is currently popular. Without the recent legalization of cannabis for medical and recreational use, many current CBD users will not get CBD-infused products legally. Though there were some studies conducted on marijuana before its legalization, such studies were not well documented. Apart from the legalization of the cannabis plant, the internet has also played a significant role in popularizing CBD. Most people these days choose to get information through the internet as it is fast. There have been many articles and videos about CBD that have been trending online. Through such articles and videos, many internet users have come to find out that CBD is beneficial.

Apart from the legalization of the cannabis plant, the internet has also played a significant role in popularizing CBD. Most people these days choose to get information through the internet as it is fast. There have been many articles and videos about CBD that have been trending online. Through such articles and videos, many internet users have come to find out that CBD is beneficial. The last reason why CBD has become popular is the health benefits it has. There has been an increasing number of people who are affirming the claims that CBD has health benefits. Some of the benefits include reducing pain and promoting good skin and mental health. Although some use CBD for recreational purposes, most CBD users use products like CBD oils and edibles for health-related reasons.

The last reason why CBD has become popular is the health benefits it has. There has been an increasing number of people who are affirming the claims that CBD has health benefits. Some of the benefits include reducing pain and promoting good skin and mental health. Although some use CBD for recreational purposes, most CBD users use products like CBD oils and edibles for health-related reasons.

Although you will part with a larger amount of money when doing a wholesale purchase, you will have saved at the end of the day because the prices will be lower. The goodness about CBD products is that they do not have a short shelf life and they also don’t require special storage conditions and you can stack them for the near future use. The retail products go for a higher price per product and you may not get a chance to test the varieties away from your usual taste.

Although you will part with a larger amount of money when doing a wholesale purchase, you will have saved at the end of the day because the prices will be lower. The goodness about CBD products is that they do not have a short shelf life and they also don’t require special storage conditions and you can stack them for the near future use. The retail products go for a higher price per product and you may not get a chance to test the varieties away from your usual taste.  Suppliers who sell CBD products at wholesale prices are usually genuine and well known because they want to maintain their reputation in the market. The wholesale products are also high-quality and you can have that guarantee unlike when you are purchasing retailers. The

Suppliers who sell CBD products at wholesale prices are usually genuine and well known because they want to maintain their reputation in the market. The wholesale products are also high-quality and you can have that guarantee unlike when you are purchasing retailers. The

A factor you should consider when choosing a logistics company is the type of resources they have. It is important to note that logistics providers don’t have access to the same number of resources. The type and size of your businesses will determine the logistics provider that will be ideal.

A factor you should consider when choosing a logistics company is the type of resources they have. It is important to note that logistics providers don’t have access to the same number of resources. The type and size of your businesses will determine the logistics provider that will be ideal. Different logistics companies tend to specialize in offering specific transportation services. Though many businesses require transport of goods they tend to focus on specific commodities. It is essential to know that some merchandise may require expertise when being transported.

Different logistics companies tend to specialize in offering specific transportation services. Though many businesses require transport of goods they tend to focus on specific commodities. It is essential to know that some merchandise may require expertise when being transported.

Brown Rice

Brown Rice

Humans know about CBD as a benefit to them but may find it alien to transpose the use of this product in animals. You still have to know that we are not the only ones who can benefit from its advantages. Currently, the documentation on the exact effects of CBD on animals is still abysmal.

Humans know about CBD as a benefit to them but may find it alien to transpose the use of this product in animals. You still have to know that we are not the only ones who can benefit from its advantages. Currently, the documentation on the exact effects of CBD on animals is still abysmal. many benefits for animals, you still have to choose it wisely and take all the necessary precautions. This is all the more important if you are making a purchase online, and it is intended for your dog or cat.

many benefits for animals, you still have to choose it wisely and take all the necessary precautions. This is all the more important if you are making a purchase online, and it is intended for your dog or cat. CBD oils for animals. There are several ways you can use CBD oil for your dogs and cats. You can use a pipette from a vial to put a few drops of the oil under your pet’s tongue. You also have the option of mixing CBD oil with your cat or dog’s diet. Choose the right type to ensure your pet is in good shape all the time.…

CBD oils for animals. There are several ways you can use CBD oil for your dogs and cats. You can use a pipette from a vial to put a few drops of the oil under your pet’s tongue. You also have the option of mixing CBD oil with your cat or dog’s diet. Choose the right type to ensure your pet is in good shape all the time.… Good services will keep the customers coming back. If customers are assured that they can always find good services, they will keep coming back and refer many to you. A business grows faster if it has satisfied customers who refer others. A satisfied customer is the best adviser you could have. The best way to market yourself to your customers is to give what you promise. Offer services that are quality and worth your customers a return on their investment.

Good services will keep the customers coming back. If customers are assured that they can always find good services, they will keep coming back and refer many to you. A business grows faster if it has satisfied customers who refer others. A satisfied customer is the best adviser you could have. The best way to market yourself to your customers is to give what you promise. Offer services that are quality and worth your customers a return on their investment. A concrete plan is needed for the success of every business and acts as an anchor. It guides and gives motivation. Take time to set goals set realistic goals based on where you want your business to be in a few years.

A concrete plan is needed for the success of every business and acts as an anchor. It guides and gives motivation. Take time to set goals set realistic goals based on where you want your business to be in a few years.

Most accidents occur because we fail to unload the gun when hunting, and some cartridge remains in the weapon. Children and unauthorized persons are the protagonists of these accidents. This occurs because the weapon is not stored in a safe place or with the percussion mechanism deactivated. Weapons should always be handled with caution.

Most accidents occur because we fail to unload the gun when hunting, and some cartridge remains in the weapon. Children and unauthorized persons are the protagonists of these accidents. This occurs because the weapon is not stored in a safe place or with the percussion mechanism deactivated. Weapons should always be handled with caution. own rules and regulations when it comes to handling weapons. Some authorities required their licensed firearm holders to keep their hunting weapons, mostly rifles, in an approved gunsmith. Cartridges, for safety, should be stored in another place away from the firearm.

own rules and regulations when it comes to handling weapons. Some authorities required their licensed firearm holders to keep their hunting weapons, mostly rifles, in an approved gunsmith. Cartridges, for safety, should be stored in another place away from the firearm. it is important to check the inside of the barrel to check that they are not obstructed by any mat or cloth, because if you do not realize it and shoot with plugged barrels, they could burst and cause a tragedy. Finally, set aside a nice and secluded area in your home to store your guns and ammunition. This should be an area that cannot be accessed easily by your kids or any other person. Follow these simple tips to avoid gun accidents.…

it is important to check the inside of the barrel to check that they are not obstructed by any mat or cloth, because if you do not realize it and shoot with plugged barrels, they could burst and cause a tragedy. Finally, set aside a nice and secluded area in your home to store your guns and ammunition. This should be an area that cannot be accessed easily by your kids or any other person. Follow these simple tips to avoid gun accidents.…

We have medical devices that have made it easier to monitor patients. It is now possible to check the progress of patients without visiting hospitals.

We have medical devices that have made it easier to monitor patients. It is now possible to check the progress of patients without visiting hospitals.

This should not bother you because different review sites will help you pick the right one. It is one thing that can make your kid happy. Understanding what your child loves most will help you choose the right toy for them. There are those who love cars, bikes, and some different toys. Take your time to know where your child’s interest lies to get what is best for them. Here are reasons why you should buy your kids nerf guns.

This should not bother you because different review sites will help you pick the right one. It is one thing that can make your kid happy. Understanding what your child loves most will help you choose the right toy for them. There are those who love cars, bikes, and some different toys. Take your time to know where your child’s interest lies to get what is best for them. Here are reasons why you should buy your kids nerf guns. Guaranteed Happiness

Guaranteed Happiness

When selecting a hybrid table saw the motor power is significant. You need to choose a saw with a powerful motor depending on the materials that you will be cutting. The most common motor power is 2.0 HP although we still have saws with 1.7 HP.

When selecting a hybrid table saw the motor power is significant. You need to choose a saw with a powerful motor depending on the materials that you will be cutting. The most common motor power is 2.0 HP although we still have saws with 1.7 HP.

It is now clear that there are many ways you can cat-proof the available outside space and there are also many methods you can use when it comes to fencing. But first, do you know the possible types of cat fence you need to buy? If no, then the following are some of the standard cat fences you are asked to recognize.

It is now clear that there are many ways you can cat-proof the available outside space and there are also many methods you can use when it comes to fencing. But first, do you know the possible types of cat fence you need to buy? If no, then the following are some of the standard cat fences you are asked to recognize.

Looking for Special Deals

Looking for Special Deals

Go Camping

Go Camping Swim in the Ocean

Swim in the Ocean

An excellent company should have a simple yet proven way of marketing and pushing traffic to your website. Note that a large percentage of people of the current generation are registered to at least one social media platform. And an SEO company that understands these facts will custom design and take advantage of this platform by coming up with a suitable method of ensuring that your company is visible on these platforms.

An excellent company should have a simple yet proven way of marketing and pushing traffic to your website. Note that a large percentage of people of the current generation are registered to at least one social media platform. And an SEO company that understands these facts will custom design and take advantage of this platform by coming up with a suitable method of ensuring that your company is visible on these platforms. Just by looking at an SEO company’s online profile, you cannot tell if the company has people who are experienced and understand the current trends and methods of pushing traffic to your site. But to know more about a company and choose the best, you need to read reviews. Excellent search engine optimization firms have a reviews section where clients post comments about the services they are receiving.

Just by looking at an SEO company’s online profile, you cannot tell if the company has people who are experienced and understand the current trends and methods of pushing traffic to your site. But to know more about a company and choose the best, you need to read reviews. Excellent search engine optimization firms have a reviews section where clients post comments about the services they are receiving.

Avoid companies that do not provide reasonable warranties. Even if long warranties are costlier than short ones, they can help you in saving money that would be spent in repairing your roof. Individuals who fail to secure a warranty will realize how its importance when their roof starts failing.

Avoid companies that do not provide reasonable warranties. Even if long warranties are costlier than short ones, they can help you in saving money that would be spent in repairing your roof. Individuals who fail to secure a warranty will realize how its importance when their roof starts failing.